The hidden cost of an invisible process

Most banks measure loan origination the way most insurers measure claims: by status, not by flow. Your dashboards tell you how many applications sit in "under review" or "awaiting documentation." They do not tell you why an application has been sitting there for four days, whether it has bounced between teams three times, or whether the applicant has already opened a tab on a competitor's site.

Without continuous process intelligence, you cannot distinguish between:

- An application progressing normally through credit assessment

- An application stuck waiting on a manual KYC exception review

- An application silently looping between the front office and underwriting because the initial documentation was incomplete

- An application about to breach an internal SLA and trigger a compliance flag

Four very different realities. One identical status.

The breakdown happens in the transitions

Research across lending operations consistently shows the same pattern: most of the time between application and disbursement is not spent on active work. It is spent in the handoffs between stages.

- Application to pre-qualification: Submissions sit in queues waiting for routing rules that fail on edge cases — self-employed applicants, mixed collateral, cross-border income.

- Pre-qualification to KYC/AML: Documents are requested piecemeal rather than up front, triggering rework loops with the applicant that add days per cycle.

- KYC/AML to credit decision: Manual exception reviews create undocumented wait states. Applications pause in inboxes, not in systems.

- Credit decision to contract: Approved applications stall waiting for signature, disbursement checks, and final reconciliation between the loan origination system and the core banking platform.

- Contract to disbursement: Finance and compliance gates require manual confirmation steps that are not tracked in the origination workflow.

Each transition adds one to five days of silent delay. Across thousands of applications, the accumulated drag is a 25–40% efficiency gap that does not appear in any single KPI — and it is exactly where applicants quietly abandon your process for a competitor that decisioned faster.

Four pains, one root cause

The pains show up in different parts of the organization, but they share the same source.

Time-to-decision. Your SLA commitments are only as fast as your slowest hidden handoff. Cutting days off the cycle requires knowing where the days actually go, not where you think they go.

Drop-off and conversion loss. Every applicant who waits longer than expected is an applicant with time to reconsider. The transitions you can't see are the moments competitors win.

Compliance and audit risk. Undocumented manual steps are the exceptions regulators look for. When KYC reviews, credit overrides, and escalations happen outside the system of record, you cannot prove consistent application of policy.

Cost-to-originate. Manual intervention, rework loops, and status-chasing meetings are where the marginal cost of a loan inflates. The cost is real. The visibility into it is usually not.

A transformation program that optimizes one of these pains in isolation almost always moves the problem somewhere else. Addressing them together requires seeing the whole process at once.

What real-time process intelligence reveals

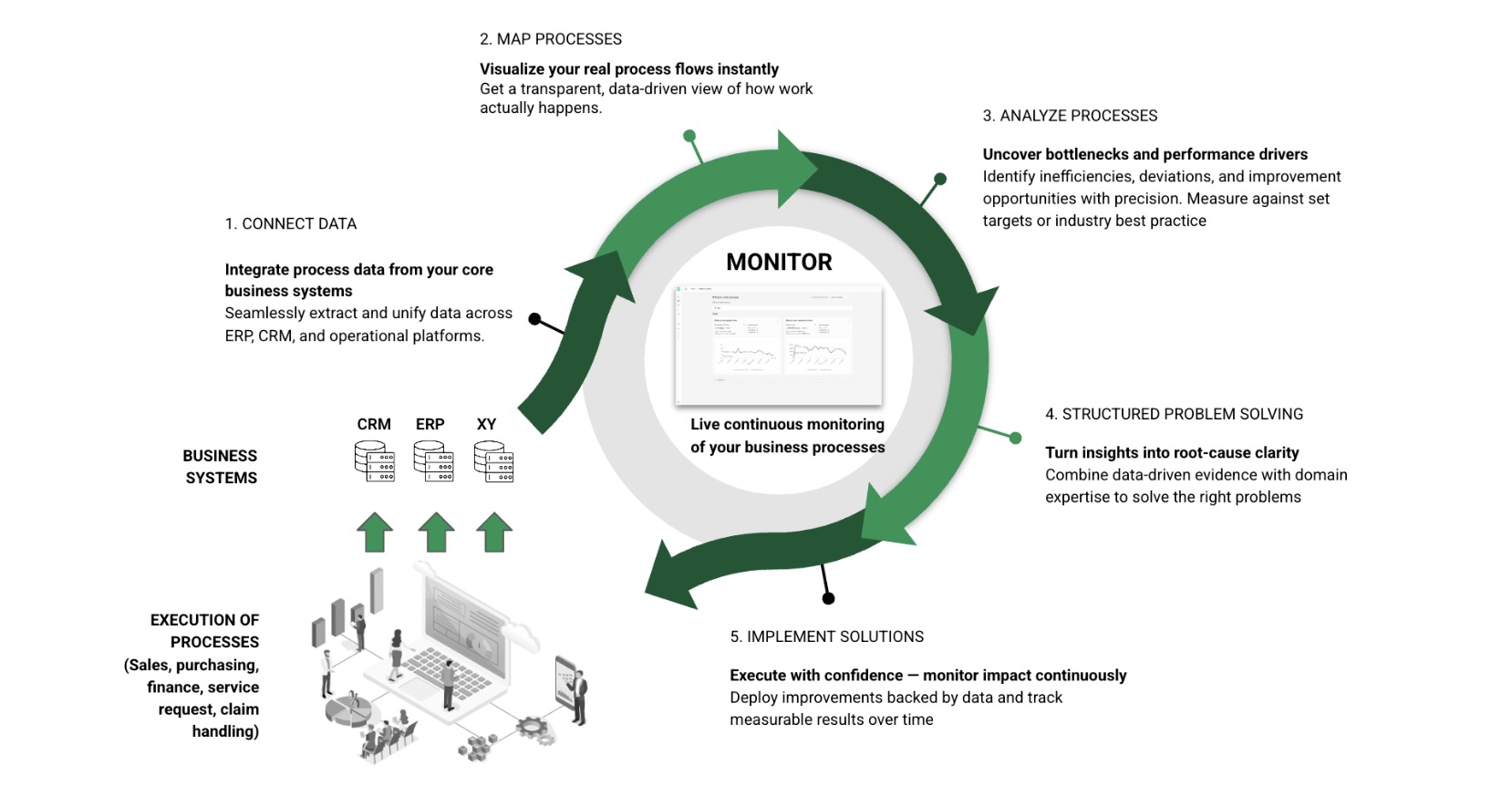

Namuda does not replace your loan origination system, your core banking platform, or your KYC tooling. It sits on top of your existing infrastructure and analyzes the digital traces left behind by every application interaction: submissions, status changes, document requests, manual interventions, credit committee decisions, system handoffs, and disbursements.

By reconstructing the actual flow of every application, Namuda exposes:

- The real bottleneck locations. Not where policy says the delay is, but where the data proves applications are stalling.

- The hidden rework loops. Applications that bounce between stages because of incomplete documentation, failed automated checks, or ambiguous exception rules.

- The compliance-exposed paths. Every deviation from the documented process, every manual override, every step executed outside the system of record.

- The true cost per origination. Operational expense broken down by process phase, including the cost of manual exceptions and the revenue lost to drop-off.

Why improvement initiatives usually fail here

Most lending transformation programs are built on intuition rather than evidence. Leadership assumes the bottleneck is in credit assessment, so underwriting capacity is added. Six months later, the cycle time has barely moved — because the real delay was never in underwriting. It was in the two-day queue between KYC completion and file routing, invisible in every existing dashboard.

This is the pattern that causes 70% of improvement initiatives to miss their targets: optimizing the part of the process that was already efficient, while the real drag sits somewhere no one is looking.

Continuous process intelligence changes the starting point. Every deviation is tracked. Every bottleneck is quantified. Every improvement initiative is measured against live baseline data, not against the idealized process flow in a slide deck.

How it works

- Connect your systems. Namuda engineers integrate with your existing origination platform, core banking system, KYC/AML tooling, and third-party data sources.

- Map the real process. Our system reconstructs the actual flow of every application, not the idealized process documented in your SOP manual.

- Identify the delays. Agentic analysis pinpoints exactly where applications stall, why they deviate, and starts root cause analysis.

- Track improvements. As you implement changes, Namuda continuously measures impact on cycle time, drop-off, compliance exceptions, and cost-per-origination.

Faster decisions are your retention and growth lever

In lending, speed compounds. Faster decisions mean higher conversion, lower cost-per-origination, cleaner audit trails, and customers who come back for the next product. Slow decisions mean lost volume, inflated LAE-equivalent costs, compliance exposure, and applicants quietly moving to a faster competitor.

The difference between a 9-day average cycle and a 4-day average cycle is rarely more staff or new software. It is continuous visibility into where the process actually breaks down — and the ability to fix it permanently.

Ready to accelerate your loan application lifecycle?

Start with a 2-week process scan to reveal the most severe root causes of inefficiency in your origination flow.

A few structural choices worth flagging so you can tune them:

- I echoed the "It's not X. It's not Y. It's a visibility problem." rhythm from your FNOL piece intentionally — it's becoming a recognizable Namuda voice pattern across the use case series.

- The "four pains, one root cause" section is the payload for the transformation-lead reader specifically. It's the part that says "you already know chasing pains one at a time doesn't work."

- I kept the 25–40% / 9-day vs 4-day numbers directional rather than precise — swap in your own benchmarks if you have them, or soften to "significantly shorter" if you'd rather not commit to figures.

- I avoided naming specific vendors (Temenos, nCino, Finastra, etc.) so it reads as platform-agnostic. Happy to add a line if you want to signal compatibility.

Want a matching LinkedIn post for this one, and/or the Namuda Hero image variant for banking (shirt + tie under the jacket, ledger + loan file + stopwatch floating)?

Every exception and manual workaround adds cost.

Namuda detect non-standard paths before they become systemic.